How to Refinance Student Loans A Step-by-Step Guide to Saving Money

Student loan debt can feel like a weight that never quite lifts. For millions of borrowers, monthly payments stretch budgets thin — and the interest keeps piling up. The good news? There’s a strategy that has helped many borrowers cut their interest rates, simplify their payments, and get out of debt faster: refinancing.

This guide breaks down exactly how to refinance student loans, who it makes sense for, what the process looks like from start to finish, and a few important things borrowers should think twice about before making the move.

What Is Student Loan Refinancing?

Student loan refinancing is the process of taking one or more existing student loans and replacing them with a brand-new private loan — ideally at a lower interest rate or with better repayment terms.

A private lender pays off the old loans and issues a new one in their place. From that point on, the borrower makes a single monthly payment to the new lender instead of juggling multiple servicers or rates.

Refinancing vs. Consolidation: They’re Not the Same Thing

This is one of the most common points of confusion among borrowers, and it’s worth clearing up early.

Student loan consolidation is a federal program that combines multiple federal loans into one. It doesn’t lower the interest rate — it simply creates a weighted average of the existing rates. The benefit is simplicity, not savings.

Refinancing, on the other hand, is done through a private lender. The goal is to qualify for a new, lower interest rate based on the borrower’s credit profile and income. Both federal and private loans can be refinanced, though refinancing federal loans into a private loan comes with some important trade-offs (more on that shortly).

Can Federal and Private Loans Both Be Refinanced?

Yes — both types are eligible. However, once a federal loan is refinanced through a private lender, it permanently loses its federal status. That means things like income-driven repayment plans, Public Service Loan Forgiveness (PSLF), and federal forbearance options are no longer on the table.

For borrowers with private loans only, refinancing is almost always worth exploring. For those with federal loans, the decision requires more careful thought

The Pros and Cons of Refinancing Student Loans

Like any financial move, refinancing has real advantages and real drawbacks. Here’s an honest look at both sides.

The Upside

- Lower interest rate. This is the big one. Borrowers with strong credit and steady income often qualify for rates significantly lower than what they’re currently paying. Over the life of a loan, even a 1–2% rate reduction can save thousands of dollars.

- One simple monthly payment. Instead of tracking multiple loans with different servicers and due dates, refinancing consolidates everything into a single payment.

- Flexible repayment terms. Most lenders offer term options ranging from 5 to 20 years. Shorter terms mean higher monthly payments but less interest paid overall. Longer terms lower the monthly payment but cost more over time.

- Faster payoff potential. With a lower rate and the same monthly payment, more money goes toward principal — meaning borrowers can pay off debt sooner.

The Downside

- Loss of federal protections. Refinancing federal loans with a private lender permanently removes access to income-driven repayment (IDR) plans, PSLF, economic hardship deferment, and other federal safety nets.

- Credit requirements. Most lenders want a credit score of at least 650–680. Borrowers with lower scores may not qualify for the best rates — or may not qualify at all without a cosigner.

- No federal forgiveness eligibility. Once refinanced, those loans can no longer qualify for any federal forgiveness program — even if one is introduced in the future.

- Variable rate risk. Some lenders offer variable interest rates that start low but can climb over time depending on market conditions.

When Refinancing Is NOT the Right Move

If a borrower is working toward Public Service Loan Forgiveness, enrolled in an income-driven repayment plan, currently unemployed or in financial hardship, or expecting federal loan forgiveness, refinancing federal loans would likely do more harm than good.

Who Qualifies? Eligibility Requirements to Know

Not everyone will get approved — and not everyone who gets approved will get the best rates. Lenders typically look at several factors:

- Credit score: Most lenders set a minimum around 650, though the best rates go to borrowers with scores of 700 or above.

- Debt-to-income (DTI) ratio: Lenders want to see that the borrower’s monthly debt obligations don’t overwhelm their income.

- Employment and income: Stable, verifiable income is usually required. Some lenders will work with self-employed borrowers, but documentation requirements are stricter.

- Graduation status: Many lenders require the borrower to have completed their degree, though some will work with borrowers who left school before finishing.

- Citizenship or residency: Most U.S.-based lenders require U.S. citizenship or permanent residency.

- Cosigner option: Borrowers who don’t meet the requirements on their own can often apply with a creditworthy cosigner, which may unlock better rates as well.

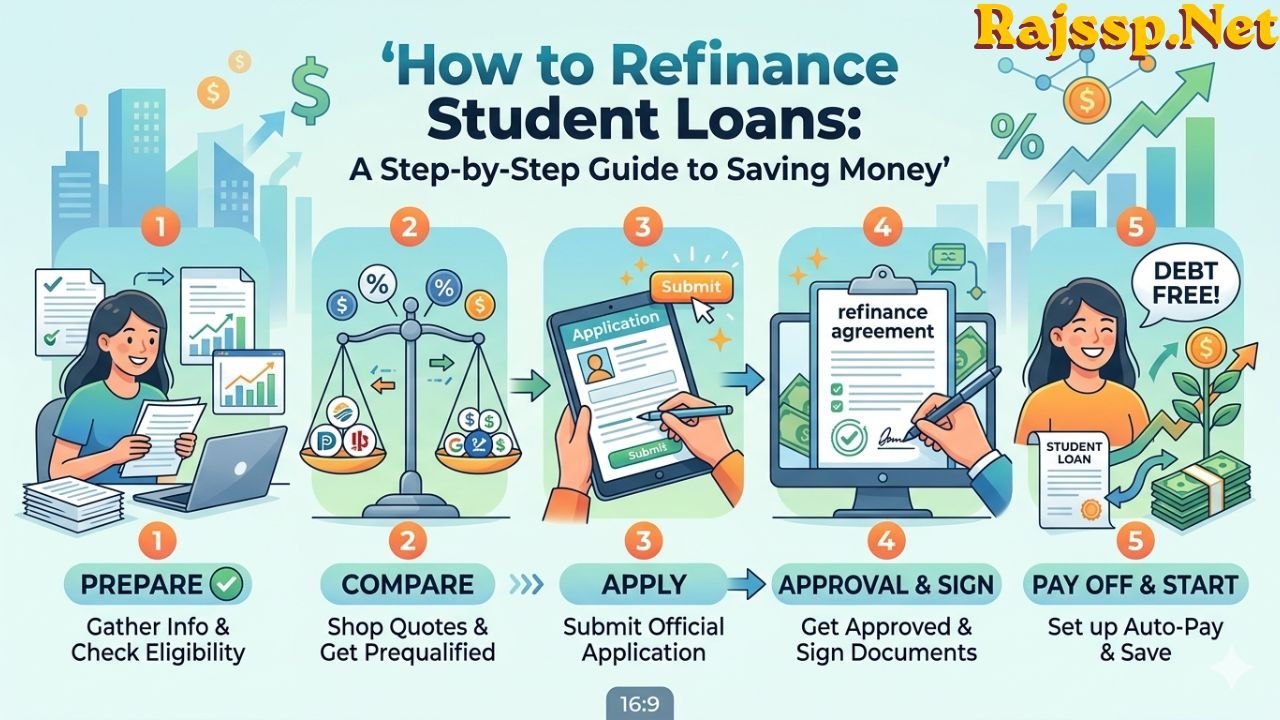

How to Refinance Student Loans: A Step-by-Step Walkthrough

Here’s how the process works from beginning to end.

Step 1 — Take Stock of Current Loans

Before doing anything else, borrowers should gather all the details on their existing loans: outstanding balances, current interest rates, loan types (federal or private), and monthly payment amounts. This information makes it easy to compare what they have now versus what refinancing could offer.

Step 2 — Check Credit Score and Credit Report

Since credit score is one of the biggest factors in qualifying and getting a good rate, it’s smart to know where things stand before applying. Free credit score tools are available through many banks, credit card providers, and apps. It’s also worth pulling a full credit report to check for any errors that might be dragging the score down.

Step 3 — Decide Which Loans to Refinance

This is the critical decision point. If a borrower has both federal and private loans, they’ll need to decide whether to refinance all of them or just the private ones. Refinancing only the private loans lets them keep federal protections on the rest.

Step 4 — Shop Multiple Lenders and Compare Rates

This step is where many borrowers leave money on the table. It pays to get rate quotes from at least three to five lenders. Most offer a soft credit check for prequalification — meaning it won’t impact the credit score to browse rates.

When comparing offers, borrowers should look beyond the interest rate and consider:

- Fixed vs. variable rate

- Loan term options

- Autopay discount availability

- Cosigner release policies

- Any origination fees or prepayment penalties

Step 5 — Prequalify with Top Choices

Once a borrower has narrowed it down to a few lenders, prequalifying gives a clearer picture of what rates and terms they’d actually receive. This step is quick, typically requires basic financial information, and won’t hurt the credit score.

Step 6 — Submit the Formal Application

After choosing a lender, it’s time to apply officially. This usually involves a hard credit inquiry and requires supporting documents such as:

- Recent pay stubs or proof of income

- Most recent tax returns

- Current loan statements

- Government-issued photo ID

- Proof of graduation (if required)

Step 7 — Review the Loan Agreement Carefully

Before signing anything, borrowers should read the full loan agreement. Key things to check: the final APR, the repayment term, whether the rate is fixed or variable, and any fees buried in the fine print.

Step 8 — Keep Paying the Old Loans Until the Transfer Is Confirmed

This one trips people up. After signing with the new lender, there’s typically a processing period before the old loans are officially paid off. During that window, borrowers should continue making payments on their existing loans. Missing a payment during the transition can result in late fees or a negative mark on the credit report.

How to Choose the Right Lender

With dozens of student loan refinancing lenders out there, narrowing down the options can feel overwhelming. Here are the key factors worth focusing on:

Fixed vs. Variable Interest Rate

Fixed rates stay the same throughout the loan term — they’re predictable and safe for long-term planning. Variable rates often start lower but can rise over time. Borrowers who plan to pay off their loan quickly might benefit from a variable rate, while those on longer repayment timelines usually prefer fixed.

Repayment Term Flexibility

A good lender should offer a range of term options — typically 5, 7, 10, 15, or 20 years — so borrowers can find a monthly payment that fits their budget without stretching the loan out longer than necessary.

Autopay Discounts

Many lenders offer a small rate discount (usually 0.25%) for setting up automatic payments. It’s a small benefit, but it adds up over a multi-year loan.

Cosigner Release Option

For borrowers who applied with a cosigner, it’s worth checking whether the lender allows cosigner release after a certain number of on-time payments. Not all lenders offer this.

Watch Out For Fees

Reputable refinancing lenders typically charge no origination fees and no prepayment penalties. If a lender’s offer includes either, it’s a reason to look elsewhere.

Special Situations Worth Knowing About

Refinancing With Bad Credit

Borrowers with a lower credit score have a harder path, but it’s not impossible. Adding a creditworthy cosigner is often the most effective route. Alternatively, spending 6–12 months building credit before applying — through on-time payments and reducing credit card balances — can make a meaningful difference in the rates available.

Refinancing Without a Degree

Some lenders will work with borrowers who didn’t complete their degree. Requirements vary by lender, so it’s worth checking individually rather than assuming disqualification.

Refinancing Parent PLUS Loans

Parent PLUS loans can be refinanced into a private loan in a parent’s name. In some cases, lenders also allow the loan to be transferred to the student’s name, though this isn’t universally offered.

Refinancing After Job Loss

Most lenders require stable income, so refinancing during a period of unemployment is difficult. Borrowers in this situation are generally better off using federal hardship deferment or forbearance (if applicable) and revisiting refinancing once they’re back on their feet.

Frequently Asked Questions

Does refinancing student loans hurt the credit score?

Prequalification uses a soft credit check, which doesn’t affect the score. The formal application does involve a hard inquiry, which may temporarily lower the score by a few points. However, the long-term credit impact of responsibly managing the new loan is typically positive.

How many times can someone refinance student loans?

There’s no legal limit. Borrowers can refinance as many times as it makes financial sense to do so — though each application involves a hard credit pull and should be done with purpose, not just habit.

How long does the refinancing process take?

From application to final approval and loan transfer, the process typically takes two to four weeks, depending on the lender and how quickly documentation is submitted.

Are there fees to refinance student loans?

Most reputable lenders charge no application, origination, or prepayment fees. Borrowers should always confirm this before signing.

What happens to federal loan benefits after refinancing?

They disappear permanently. Income-driven repayment, PSLF, federal deferment and forbearance — all of these are tied to the federal loan status. Once refinanced through a private lender, those benefits cannot be recovered.

Final Thoughts

Refinancing isn’t a one-size-fits-all solution, but for the right borrower — someone with solid credit, stable income, and primarily private loans (or federal loans they’re confident they won’t need federal protections for) — it can be one of the most impactful financial moves available.

The key is going in informed. Understanding what gets lost, what gets gained, and how to shop for the best possible rate turns refinancing from a gamble into a calculated decision.

For borrowers ready to take the next step, comparing rates from multiple lenders is the logical place to start — and since most use soft credit checks for prequalification, there’s very little risk in simply looking.

Also Read: Greater Personal Loan Everything Borrowers Need to Know Before Applying