Flot Loan Explained: What It Is, How It Works, and Is It Right for You?

Most people hear the word “loan” and think of a single, straightforward concept — borrow money, pay it back. But the world of lending is far more nuanced than that. Flot loans, for instance, are one of those financial tools that can either save a borrower a significant amount of money or catch them off guard if they’re not prepared. Whether someone is a first-time borrower, a small business owner trying to manage cash flow, or a finance student trying to wrap their head around lending structures, understanding what a flot loan is and how it works can make a real difference in making smart financial decisions.

This article breaks down flot loans in plain language — what they are, the different types, how they compare to fixed-rate loans, and how to figure out whether one might be the right fit.

What Is a Flot Loan?

At its most technical, a flot loan — sometimes called “interim financing” — is a short-term loan with a maximum term of 30 months, drawn from funds that have been obligated but not yet spent. This definition is often used in the context of government programs or structured lending arrangements.

But in everyday financial language, the term carries a broader meaning. To “flot a loan” simply means to obtain a loan from a financial institution, or in some cases, to allow someone else to borrow money. Think of phrases like “the company floted a loan to cover unexpected expenses” — that’s the general usage most people encounter.

There’s also an important distinction worth clearing up right away: “floting a loan” (the act of taking or giving a loan) is not the same thing as a “floting-rate loan” (a specific type of loan where the interest rate changes over time). Both fall under the umbrella of flot loan concepts, but they refer to different things. Understanding this difference is the first step toward navigating this topic confidently.

Types of Flot Loans

Flot loans aren’t a one-size-fits-all product. They come in several forms, each with its own structure and use case.

Floting-Rate Loans

A floting-rate loan is a business or personal loan where the interest rate doesn’t stay the same throughout the life of the loan. Instead, it shifts based on market conditions. This means that a borrower’s monthly payments can go up or down over time, depending on what’s happening in the broader economy.

This type of loan is especially common in business financing. Companies that need capital but want to take advantage of potentially falling interest rates often opt for floting-rate structures rather than locking themselves into a fixed rate.

Flot Period Loans

A flot period loan works a bit differently. Here, the “flot” refers to a window of time — usually a specific number of days — during which no interest is charged on the borrowed amount. This flot period typically sits between the date the loan is disbursed and the date the first payment is due.

For borrowers, this grace-like window can be a helpful buffer, giving them time to put the funds to use before repayment kicks in.

Syndicated Floting-Rate Loans

At the more complex end of the spectrum sit syndicated floting-rate loans. These are a form of debt financing that’s typically negotiated between a group of banks and a corporation. They’re often extended to companies that carry higher levels of debt relative to their cash flow — which means they come with a greater credit risk compared to investment-grade bonds.

Syndicated loans are a cornerstone of large-scale corporate financing, often structured over several years with floating rates that adjust to reflect market conditions.

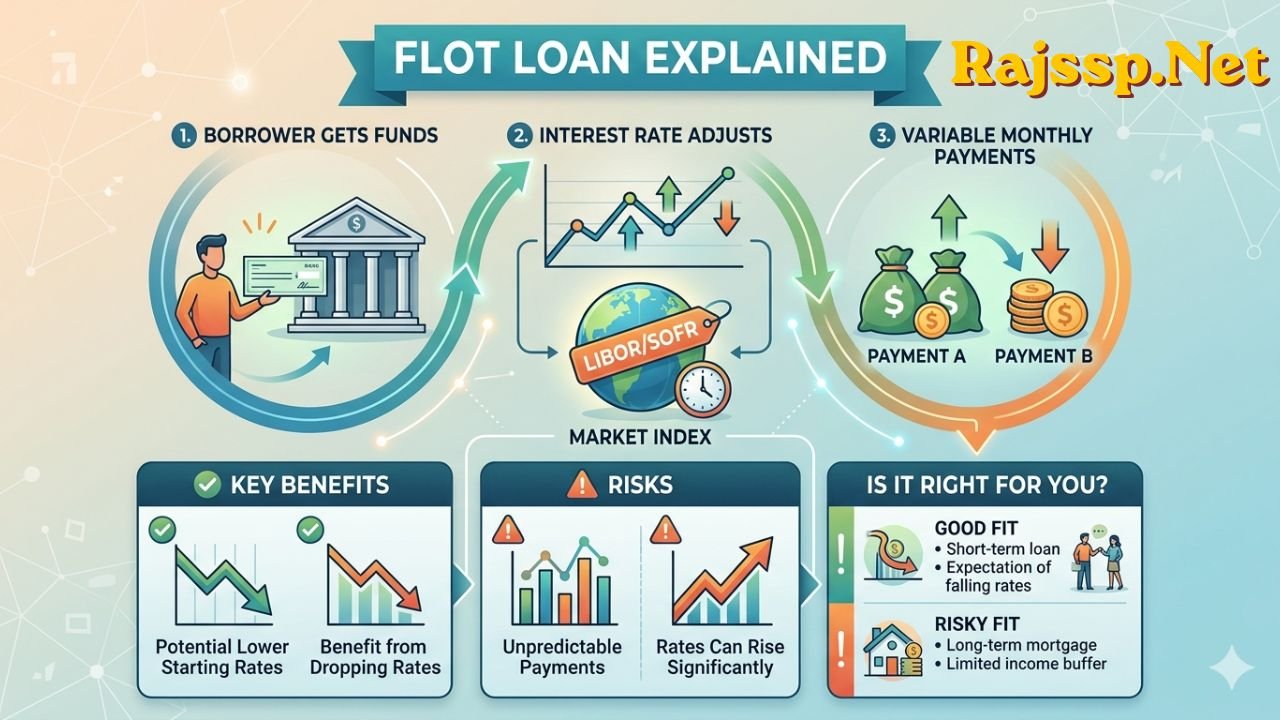

How Flot Loans Work

Understanding the mechanics of a flot loan helps borrowers avoid surprises down the road.

How Interest Rates Are Set and Adjusted

With a floting-rate loan, the interest rate isn’t chosen arbitrarily. It’s typically tied to a recognized market benchmark — a reference point that reflects current lending conditions. Common benchmarks include the prime rate, the London Interbank Offered Rate (LIBOR), and the federal funds rate. The loan’s interest rate is usually expressed as the benchmark rate plus a fixed margin or “spread” — for example, prime rate plus 2%.

The rate on a flot loan can be adjusted quarterly, half-yearly, or annually, depending on the terms agreed upon at the outset. Borrowers are supposed to be informed promptly whenever an adjustment takes place, so they can plan their finances accordingly.

The Reset Cycle

The periodic reset of the rate — typically happening quarterly or semi-annually — is what makes floting-rate loans inherently dynamic. A borrower’s debt service cost isn’t locked in the way it would be with a fixed-rate product. Each reset period, the lender recalculates the interest owed based on the updated benchmark, and the payment amount adjusts accordingly.

This reset cycle is what creates both the appeal and the risk of flot loans. In a falling rate environment, it’s a significant advantage. In a rising rate environment, it can squeeze a borrower’s budget.

Flot Loan vs. Fixed-Rate Loan

One of the most common questions people have when exploring flot loans is: how do they compare to fixed-rate loans? The answer depends a lot on the borrower’s situation and the state of the market.

With a fixed-rate loan, a borrower pays the same amount every single month for the entire term of the loan, regardless of what happens in the broader economy. If rates go up, the fixed-rate borrower doesn’t feel it. If rates go down, they don’t benefit either.

With a floting rate, the picture is different. Payments could rise or fall throughout the life of the loan depending on how the benchmark rate moves. Here’s a simple way to think about it:

A fixed-rate loan offers stability — but at the cost of flexibility. A borrower locks in a predictable payment, which makes budgeting straightforward. However, they give up the opportunity to pay less if interest rates drop during the loan term.

A floting-rate loan offers potential savings — but comes with uncertainty. If rates fall, a borrower benefits directly. If rates rise, their payments go up, sometimes significantly.

When to Choose Each

A fixed-rate loan tends to make more sense when rates are low and expected to rise, when a borrower needs payment predictability, or when the loan term is long. A flot loan tends to make more sense when rates are high and expected to fall, when the borrower has a shorter loan term, or when they have the financial cushion to absorb potential payment increases.

Pros and Cons of Float Loans

Like any financial product, flot loans come with their own set of advantages and disadvantages. Here’s an honest look at both sides.

Advantages

Potential for lower payments. When market interest rates fall, borrowers with flot loans directly benefit. Their payments decrease without having to refinance or renegotiate the loan — it happens automatically through the rate reset process.

Historical cost advantage. Looking back over any 30-year period in history, floting rates have, on average, tended to be the cheaper option compared to fixed rates. This doesn’t guarantee future results, but it does suggest that over the long run, floting-rate borrowers have often come out ahead.

Flexibility for short-term borrowers. For someone who doesn’t plan to carry the loan for its full term — perhaps they expect to repay it early or refinance — a flot loan can offer lower initial costs without the long-term risk that longer-term borrowers face.

Disadvantages

Payment unpredictability. The biggest drawback of a flot loan is that monthly payments can change. For someone managing a tight budget, this unpredictability can be genuinely stressful and difficult to plan around.

Market risk exposure. Allowing the rate to flot exposes the borrower to market risk. When benchmark rates climb, so do payments — sometimes faster and higher than expected. There’s also a risk of being disadvantaged by lenders who adjust rates in ways that don’t fully reflect market movements in the borrower’s favor.

Difficult to budget long-term. Businesses and individuals alike often find it hard to make accurate long-term financial projections when a core cost — loan repayment — is a moving target.

Who Uses Flot Loans?

Flot loans are used across a wide spectrum of borrowers, from individuals managing everyday financial needs to large corporations handling billion-dollar financing rounds.

Individual borrowers may encounter flot loans in the form of adjustable-rate mortgages (ARMs) or variable-rate personal loans. These can be attractive at the outset due to lower initial rates.

Small and mid-sized businesses often use floting-rate loans to manage working capital — covering payroll, inventory, or operational expenses — particularly when they expect cash flow to improve and want to take advantage of any rate drops.

Large corporations access floting-rate financing through syndicated loan markets, where groups of banks collectively fund large credit facilities for companies with significant capital needs.

Government and public sector entities may use flot loans in the form of interim financing — drawing from committed but unused funds to bridge gaps in project timelines, as seen in programs like the Canada Emergency Business Account (CEBA).

Key Terms to Know

Before diving into a flot loan agreement, it helps to be familiar with the terminology. Here’s a quick reference:

Benchmark rate / reference rate — The market index to which a floting loan’s interest rate is tied (e.g., prime rate, LIBOR, SOFR).

Spread / margin — The fixed percentage added to the benchmark rate to determine the borrower’s actual interest rate.

Rate reset period — The interval at which the interest rate is recalculated and adjusted (e.g., quarterly, semi-annually, annually).

Loan prime rate (LPR) — A key reference rate used particularly in Chinese financial markets for floting-rate loan agreements in international commerce.

Flot period — A defined window of time after loan disbursement during which no interest is charged.

Interim financing — Another name for a short-term flot loan, often used in real estate or project-based lending contexts.

How to Decide If a Flot Loan Is Right for You

Choosing between a flot loan and a fixed-rate loan is a personal financial decision, and there’s no universal right answer. Here are a few questions worth considering:

What is your risk tolerance? If the idea of variable monthly payments causes stress, a fixed-rate loan might be a better psychological fit — even if a flot loan could save money over time.

What is the current interest rate environment? If rates are historically high and expected to come down, a flot loan positions a borrower to benefit. If rates are low and expected to rise, locking in a fixed rate might be smarter.

How long is the loan term? Short-term borrowers face less risk with floting rates because there’s simply less time for rates to shift dramatically. Long-term borrowers carry more exposure.

Is professional advice available? Anyone who is uncertain about which option suits their situation would do well to speak with a financial advisor or loan specialist. These decisions have real, lasting financial consequences, and a professional can help weigh the specifics of an individual’s situation.

Conclusion

Flot loans are a fascinating and genuinely useful corner of the lending world — but they’re not for everyone. For borrowers who understand how they work, have the financial flexibility to handle payment changes, and are entering a rate environment that favors variable structures, a flot loan can be a smart and cost-effective choice. For those who value stability above all else, a fixed-rate product might be the better path.

The most important takeaway is this: knowledge is protection. Understanding the difference between floting and fixed rates, knowing what benchmark rates are and how they influence payments, and being honest about one’s own financial situation are the building blocks of a sound borrowing decision.

Anyone considering a flot loan should compare options carefully, ask lenders the right questions, and never hesitate to seek professional guidance. The right loan structure can make a meaningful difference — not just in monthly payments, but in long-term financial wellbeing.

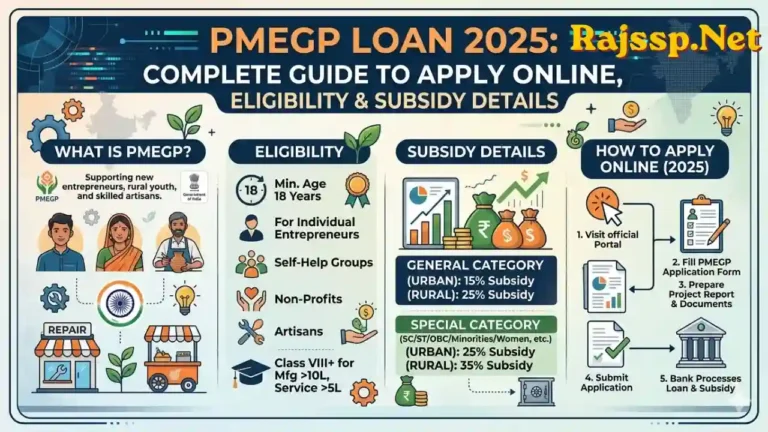

Also Read: PMEGP Loan 2025 Complete Guide to Apply Online, Eligibility & Subsidy Details