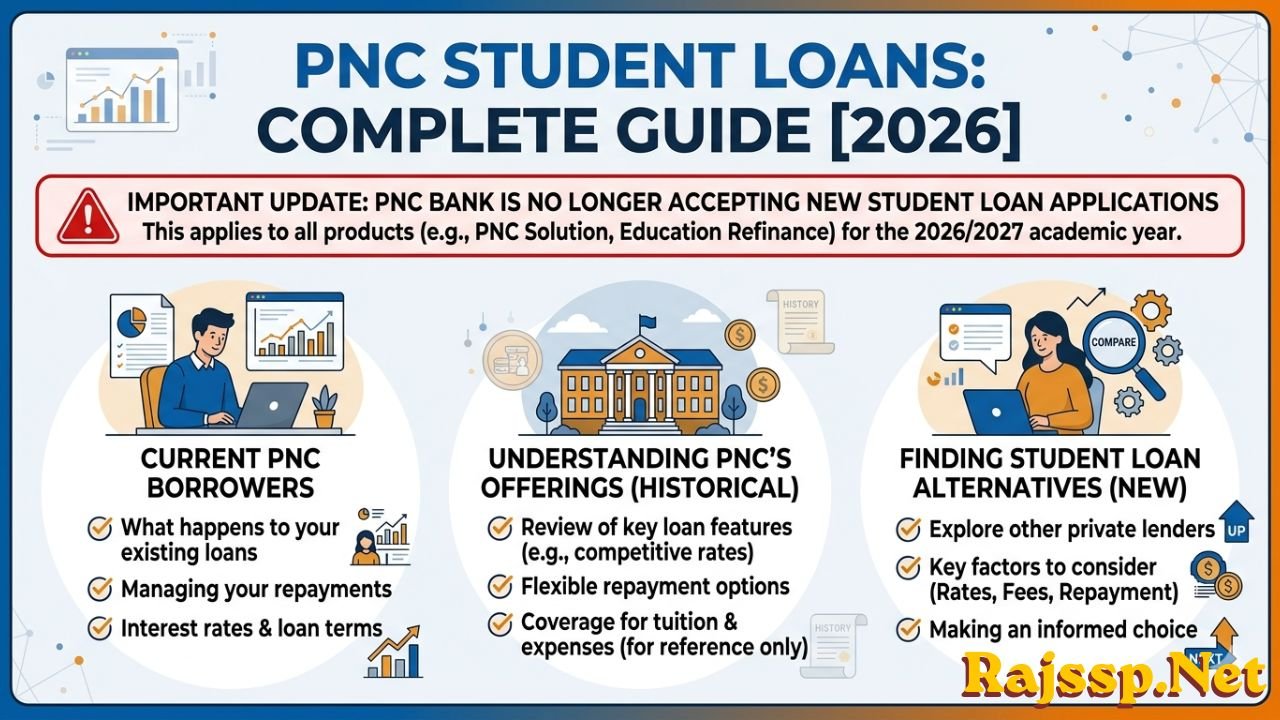

PNC Student Loans: Complete Guide [2026]

Introduction

When it comes to private student lending in the United States, PNC Bank has long been a recognizable name. For years, PNC Bank student loans have helped thousands of undergraduate and graduate students cover tuition, housing, and other school-certified expenses. The bank offered competitive rates, flexible repayment options, and a range of loan types tailored to different academic paths.

However, there’s an important update every borrower and prospective applicant needs to know: as of December 18, 2025, PNC Bank is no longer accepting new student loan applications — including applications for the 2026/2027 academic year. This applies to all PNC student loan products, including the PNC Solution Student Loan and the PNC Education Refinance Loan.

This guide is for three groups of people: current PNC borrowers who need to understand what happens to their existing loans, researchers who want a full picture of what PNC bank student loans offered, and new borrowers who are now looking for the right alternative. Let’s break it all down.

What Were PNC Student Loans? (Overview)

PNC’s History as a Private Student Loan Provider

PNC Financial Services Group is one of the largest banks in the United States, with a strong presence in personal and commercial banking. For many years, PNC bank offered private student loans as a complement to federal aid — helping students bridge the gap between what federal loans covered and what their education actually cost.

The bank’s student lending portfolio grew to include loans for students at virtually every stage of their academic journey, from undergraduate freshmen to medical residents sitting for board exams. PNC’s loans were available in all 50 states, making them one of the more accessible private lenders in the country.

Types of PNC Student Loans Offered

Before the program was discontinued, PNC offered a diverse lineup of student loan products under the PNC Solution Loan brand:

- Undergraduate PNC Solution Student Loan — Designed for students pursuing a four-year degree, this was the most widely used PNC student loan product.

- Graduate Student Loans — Available for students enrolled in master’s, doctoral, and other graduate-level programs.

- Health & Medical Professions Loans — Tailored for students in medical, dental, pharmacy, and other healthcare programs.

- Health Professions Residency Loans — A specialized loan product for medical graduates entering residency programs.

- Bar Study Loans — Offered to law school graduates preparing for the bar exam.

- PNC Education Refinance Loan — Allowed borrowers to consolidate and refinance both federal and private student loans into a single private loan.

All of these products were available to eligible borrowers across all 50 states, making PNC bank student loans a widely accessible option for American students.

PNC Student Loan Rates & Terms

Interest Rates on PNC Solution Student Loans

One of the main reasons students considered PNC student loans was the competitive rate structure. The PNC Solution Student Loan APR interest rate 2025 figures, as officially published, were as follows:

- Variable APR: 5.64% – 13.39%

- Fixed APR: 4.49% – 12.24%

These PNC solution student loan APR interest rate 2025 figures already reflected a 0.50% autopay discount, which was applied when borrowers set up automated payments through AES (American Education Services). If a borrower did not enroll in autopay, rates would be 0.50% higher than the advertised figures.

The PNC solution student loans APR interest rate 2025 rates were considered competitive within the private student loan market, particularly for borrowers with strong credit histories or a creditworthy cosigner.

Loan Amount Ranges

PNC bank student loans came with defined borrowing limits depending on the student’s level of study:

- Undergraduate students: $50,000 – $75,000 per year (up to $225,000 total lifetime limit)

- Graduate students: Up to $350,000 total (inclusive of both federal and private student loan debt)

The minimum loan amount was $1,000, and all funds were disbursed directly to the school.

Repayment Terms

Borrowers could choose from repayment terms of 5, 10, or 15 years for standard PNC student loans. For the PNC Education Refinance Loan, repayment terms extended up to 20 years. The flexibility in term length allowed borrowers to balance monthly payment affordability against total interest paid over time.

Repayment Options

In-School Repayment Choices

PNC bank student loans stood out for offering three distinct in-school repayment options, giving borrowers real flexibility based on their financial situation during school:

- Immediate Repayment — Begin making full principal-and-interest payments right away while still enrolled.

- Interest-Only Payments — Pay only the accruing interest while in school to prevent loan balance growth.

- Full Deferment — Postpone all payments until six months after leaving school (the grace period).

Borrowers who started repayment early — especially through interest-only payments — could significantly reduce their total loan cost by the time they graduated.

Grace Period

For borrowers who chose deferment, PNC provided a six-month grace period after leaving school before full repayment was required. During this time, interest continued to accrue and was typically capitalized at the end of the grace period.

Cosigner Release

One of the more borrower-friendly features of PNC bank student loans was the cosigner release option. After making 48 consecutive on-time monthly payments (or fewer in some states, as required by law), the primary borrower could apply to have the cosigner removed from the loan. This was a meaningful benefit for undergraduate borrowers who often needed a parent or guardian as a cosigner to qualify.

Eligibility Requirements

Basic Borrower Requirements

To qualify for a PNC student loan, both the borrower and any cosigner were required to meet specific criteria. According to PNC’s official requirements, borrowers and cosigners must be U.S. citizens or permanent resident aliens, and the student must be enrolled at least half-time at an eligible institution.

International students were only eligible if they held a green card or a valid U.S. visa and applied with a qualified cosigner who met the citizenship requirements.

Credit and Income Requirements

PNC did not publicly disclose a minimum credit score for their student loan products. However, based on third-party data, an approximate minimum credit score of around 600 was considered the baseline for approval. In practice, the best rates were typically reserved for borrowers with scores well above that threshold.

Borrowers and cosigners were also required to:

- Provide employment information

- Meet a qualifying debt-to-income ratio

- Demonstrate satisfactory overall credit history

Because no soft credit prequalification was available, any application triggered a hard credit inquiry — a notable downside for borrowers who wanted to rate-shop without affecting their credit score.

PNC Education Refinance Loan (PNC Bank Student Loan Refinance)

What Is It?

The PNC Education Refinance Loan — often referred to as the PNC student loan refinance product or PNC bank student loan refinance option — was designed to help graduates consolidate multiple loans into one. Whether a borrower had federal loans, private PNC loans, or a mix of both, the PNC refinance student loans program allowed them to roll everything into a single monthly payment with a potentially lower interest rate.

Rates and Terms

The PNC bank student loan refinance product offered both fixed and variable interest rate options, with repayment terms of 5, 10, 15, or 20 years. A longer term lowered monthly payments but increased total interest paid; a shorter term did the opposite.

Refinance loan amounts ranged from $10,000 to $200,000, depending on the borrower’s degree type and graduation status. Borrowers who had not yet graduated could still qualify for PNC refinance student loans, though they faced a lower borrowing cap of $25,000 and needed at least 24 months of repayment history.

An Unusual Advantage

Notably, PNC allowed refinancing for non-graduates — a relatively uncommon feature in the private refinancing market. Most lenders require proof of graduation before approving a refinance application, so this made the PNC bank student loan refinance product more inclusive.

A Critical Warning About Refinancing Federal Loans

Anyone considering a PNC student loan refinance of federal loans should understand the serious trade-offs involved. Once federal student loans are refinanced into a private loan, the borrower permanently loses access to:

- Income-driven repayment plans (IBR, PAYE, SAVE)

- Federal forgiveness programs (Public Service Loan Forgiveness, Teacher Loan Forgiveness)

- Federal forbearance and deferment protections

For this reason, PNC refinance student loans — or any private refinance, for that matter — were best suited for borrowers with stable incomes who were confident they would not need federal protections in the future.

Pros & Cons of PNC Student Loans

Pros

- No application or origination fees — Borrowers paid nothing upfront to apply.

- Autopay discount of 0.50% — A better-than-average rate reduction for enrolling in automatic payments.

- Cosigner release available — After 48 months of on-time payments, cosigners could be removed.

- Specialized loan products — Tailored options for medical students, health profession residents, and bar exam candidates.

- In-house loan servicing — PNC serviced its own loans through AES, meaning borrowers generally dealt with a consistent servicer throughout the loan’s life.

- Rated A+ by the Better Business Bureau — A strong institutional reputation.

Cons

- No longer accepting new applications — As of December 18, 2025, PNC bank student loans are no longer available to new applicants.

- Credit requirements not publicly disclosed — Lack of transparency made it hard to know before applying whether one would qualify.

- No prequalification option — Applying required a hard credit pull, which could affect the borrower’s credit score.

- “Bad” customer service rating on Trustpilot — Based on approximately 2,000 reviews, PNC received a poor rating from borrowers regarding service quality.

- Not eligible for federal forgiveness programs — As private loans, PNC student loans never qualified for federal relief, including income-driven repayment forgiveness or PSLF.

- Late fees applied — A fee equal to 5% of the missed payment or $5 (whichever was lower) was assessed for payments received more than 15 days past the due date.

What Happens to Existing PNC Student Loan Borrowers?

If someone already has a PNC student loan, there’s no reason to panic. PNC has been clear about what existing borrowers can expect following the discontinuation of new applications.

Existing PNC bank student loans will continue to be serviced by American Education Services (AES) or Aspire — the same servicers that have always handled PNC’s loan portfolio. Borrowers do not need to take any action. Their loan terms and conditions remain exactly as stated in their original Credit Agreement and Final Disclosure documents.

Here’s what won’t change for existing PNC student loan borrowers:

- Servicer — Loans stay with AES or Aspire; no transfer is happening.

- Loan terms — Interest rates and repayment schedules remain unchanged.

- Deferment — Any in-school or hardship deferment processes are not affected.

- Repayment — Borrowers should continue making payments as required.

One thing that will not happen: the discontinuation of new applications does not give borrowers an automatic option to transfer or move their current loans to another lender. If someone wants to refinance their existing PNC student loan elsewhere, they would need to apply independently with a new lender.

For general questions, borrowers can contact PNC directly at 1-800-762-1001 (Monday–Friday, 8 a.m.–5 p.m. ET). For servicing questions, AES can be reached at 800-233-0557 (Monday–Friday, 7:30 a.m.–9:00 p.m. ET).

PNC Student Loan Alternatives (Best Options in 2026)

Since PNC bank student loans are no longer available, new borrowers need to look elsewhere. The good news is that there are several strong private lenders in the market. Here are the top alternatives to consider:

College Ave Student Loans — Known for a wide variety of repayment term options (5–20 years) and a fully online application process. A strong choice for undergrads and grad students alike.

Earnest — Offers flexible repayment, the ability to skip one payment per year, and merit-based underwriting that considers more than just credit score.

Sallie Mae — One of the largest private student lenders in the country, with loan products for nearly every academic stage, including career training and part-time students.

ELFI (Education Loan Finance) — Particularly strong for refinancing, with competitive rates and a dedicated personal loan advisor assigned to each borrower.

SoFi — A well-rounded lender offering student loans, refinancing, and membership benefits like career coaching and unemployment protection.

When comparing any of these alternatives, borrowers should weigh the following key factors:

- Interest rates (fixed vs. variable, and the range offered)

- Repayment term flexibility

- Cosigner options and cosigner release policies

- Hardship protections (forbearance, deferment, income-based options)

- Availability of prequalification (to check rates without a hard credit pull)

PNC Student Loans vs. Federal Student Loans

Understanding the difference between PNC bank student loans and federal student loans is essential for any borrower making financial decisions.

Key Differences

| Feature | PNC Student Loans (Private) | Federal Student Loans |

|---|---|---|

| Eligibility | Credit-based | Based on FAFSA (no credit check for most) |

| Interest Rates | Variable or fixed, credit-dependent | Fixed, set by Congress |

| Repayment Flexibility | Limited | Income-driven repayment plans available |

| Forgiveness Programs | None | PSLF, IDR forgiveness, Teacher Forgiveness |

| Forbearance/Deferment | Limited options | Broad federal protections |

| Cosigner | Often required | Not required (except PLUS Loans) |

Federal Benefits Not Available with Private Loans

PNC student loans, like all private loans, did not qualify for any federal programs. Borrowers who refinanced federal loans into PNC bank student loans permanently lost access to income-driven repayment (IBR, PAYE, SAVE), Public Service Loan Forgiveness (PSLF), and generous federal forbearance and deferment options. This is a critical distinction that borrowers should never overlook.

When to Choose Private Over Federal

Private loans like PNC student loans were generally the right choice only after exhausting all federal aid. They made sense when a borrower had maximized their federal loan eligibility, had strong credit (or a qualified cosigner), and needed additional funds to cover remaining school costs. They were not the right fit for borrowers planning on careers in public service, nonprofit work, or any field where PSLF could eventually eliminate loan balances.

Frequently Asked Questions (FAQ)

Are PNC student loans still available?

No. As of December 18, 2025 at 10:00 a.m. EST, PNC is no longer accepting new student loan applications. This includes all PNC Solution Student Loan products and the PNC Education Refinance Loan. Applications created before that date were given up to 30 additional days to complete and submit.

What happens to my existing PNC student loan?

Existing PNC bank student loans are not affected. They continue to be serviced by AES or Aspire, and all loan terms remain exactly as originally agreed. Borrowers should keep making payments as required and reach out to their servicer (not PNC directly) for repayment-related questions.

Can I refinance my PNC student loan elsewhere?

Yes. Borrowers with existing PNC student loans can apply to refinance with another private lender. Lenders like ELFI, Earnest, SoFi, and College Ave all accept applications from borrowers looking to refinance existing private student loans. It’s important to compare rates and terms carefully before deciding.

Did PNC student loans qualify for federal forgiveness?

No. PNC student loans are private loans. Private student loans do not qualify for any federal programs, including income-driven repayment forgiveness, Public Service Loan Forgiveness, or any other Department of Education relief programs.

How do I contact PNC about my student loan?

For general questions about existing accounts or active applications: 1-800-762-1001, Monday–Friday, 8 a.m.–5 p.m. ET. For servicing-related questions, contact AES at 800-233-0557, Monday–Friday, 7:30 a.m.–9:00 p.m. ET, or Aspire at their customer service line, Monday–Friday, 8 a.m.–6 p.m. CT.

Conclusion

PNC bank student loans were, for many years, a reputable and competitive option in the private student lending space. The PNC Solution Student Loan offered flexible repayment, no origination fees, and tailored products for undergraduates, graduate students, healthcare professionals, and law graduates. The PNC student loan refinance product gave borrowers a meaningful way to consolidate and potentially lower the cost of their education debt.

But with PNC no longer accepting new applications as of December 2025, the landscape has changed. Existing borrowers can rest easy — their loans are safe, their terms are unchanged, and AES or Aspire will continue to service them without disruption.

For new borrowers, the priority should be the same as it always was: exhaust federal student loan options first, then compare private lenders carefully. College Ave, Earnest, SoFi, Sallie Mae, and ELFI are all worth exploring as alternatives to PNC bank student loans in 2026.

The right loan depends on the borrower’s credit profile, career path, and long-term financial goals. Shop smart, compare rates, and never refinance federal loans into private ones without fully understanding what’s being given up.

Also Read: Dot Dot Loans: What It Was, What Happened, and the Best Alternatives in 2026