PMEGP Loan 2025 Complete Guide to Apply Online, Eligibility & Subsidy Details

Starting a business from scratch can feel overwhelming, especially when funding is the biggest barrier. That’s exactly where the PMEGP loan steps in. This government-backed scheme has been quietly changing lives across India — helping young entrepreneurs, rural youth, and skilled artisans turn their business ideas into reality. Whether someone has heard about it recently or has been searching for reliable PMEGP loan details, this guide covers everything from scratch.

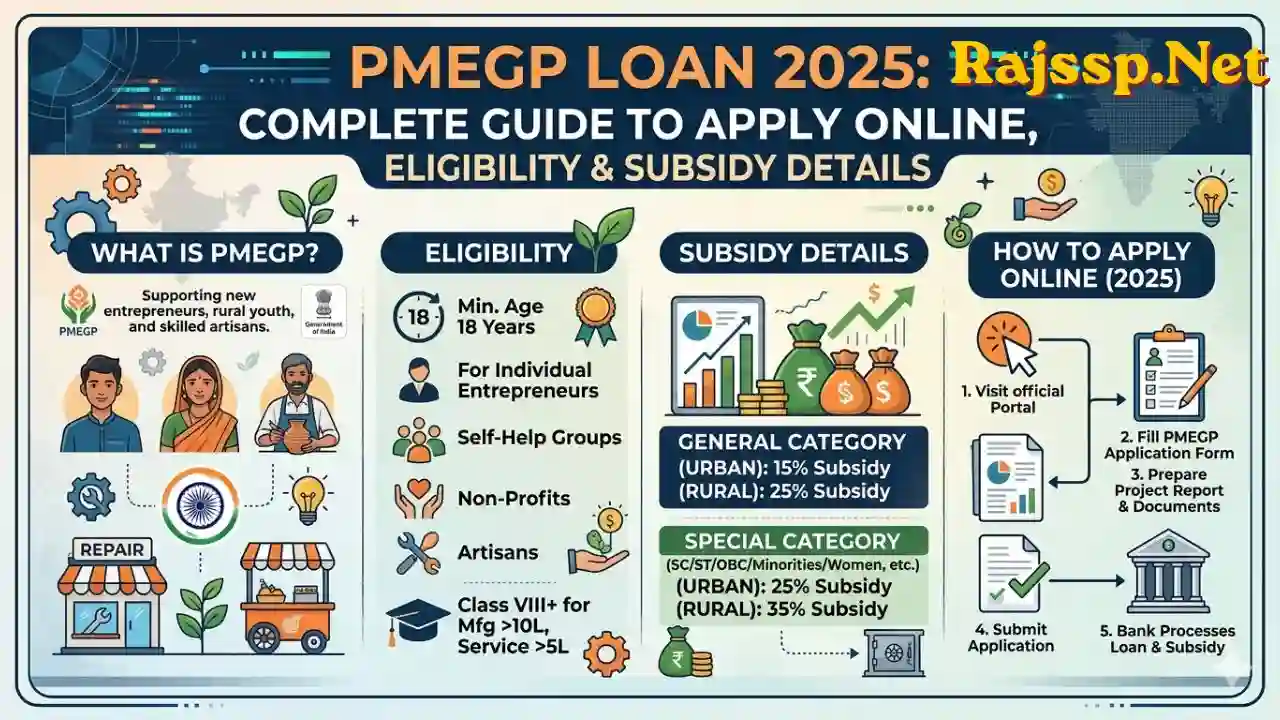

What Is the PMEGP Loan Scheme?

The PMEGP loan scheme — short for Prime Minister’s Employment Generation Programme — is a flagship credit-linked subsidy initiative run by the Ministry of Micro, Small and Medium Enterprises (MoMSME), Government of India. It was launched in 2008 by merging two older programs: PMRY (Prime Minister’s Rojgar Yojana) and REGP (Rural Employment Generation Programme).

At its core, the PMEGP loan yojana is designed to do one thing well — help unemployed individuals set up their own micro-enterprises and generate sustainable employment, both for themselves and others in their communities. The scheme is implemented at the national level by the Khadi and Village Industries Commission (KVIC), while State KVIC offices, State Khadi & Village Industries Boards (KVIBs), and District Industries Centres (DICs) assist at the ground level.

What makes the PMEGP loan govt scheme stand out is its blend of a bank loan and a government subsidy. Applicants don’t just receive borrowed money — a significant chunk of the project cost is covered by the government as a margin money subsidy, reducing the financial burden considerably.

PMEGP Loan Scheme 2022 to 2025–26: Key Updates

The PMEGP loan scheme 2022 marked a significant phase in the programme’s evolution. The government extended and enhanced the scheme for the 15th Finance Commission cycle, covering five years from 2021–22 to 2025–26, with a total outlay of ₹13,554.42 crore.

Some of the most important updates include:

- The maximum project cost for manufacturing units has been revised upward from ₹25 lakh to ₹50 lakh

- For service-based units, the limit has been raised from ₹10 lakh to ₹20 lakh

- Transgender applicants now qualify for special category benefits with a higher subsidy rate

- The Union Budget 2025 introduced enhanced credit guarantees and tax benefits for MSMEs and startups, further strengthening the PMEGP framework

PMEGP Loan Eligibility: Who Can Apply?

Before thinking about how to apply for a PMEGP loan, it’s important to confirm whether one qualifies. Here’s a clear breakdown of PMEGP loan eligibility:

- The applicant must be an Indian citizen

- Minimum age: 18 years — there is no upper age limit

- For manufacturing projects above ₹10 lakh and service projects above ₹5 lakh, the applicant must be at least 8th standard pass

- The loan is strictly for new businesses only — existing businesses or units already receiving government subsidies are not eligible

- Self-help groups (SHGs), charitable trusts, and institutions registered under the Societies Registration Act, 1860 are also eligible

- Cooperative societies engaged in non-farm activities may also apply

One key point worth noting: anyone who has already benefited from any other government subsidy scheme cannot apply for the PMEGP loan simultaneously.

PMEGP Loan Subsidy Details: How Much Does the Government Cover?

Understanding the PMEGP loan subsidy details is perhaps the most important part of the entire scheme. The subsidy varies based on two factors — the applicant’s category (General or Special) and their location (Urban or Rural).

Here’s how it works:

General Category:

- Rural areas: 25% subsidy, 10% self-contribution

- Urban areas: 15% subsidy, 10% self-contribution

Special Category (SC/ST/OBC, women, minorities, ex-servicemen, physically challenged, transgender):

- Rural areas: 35% subsidy, 5% self-contribution

- Urban areas: 25% subsidy, 5% self-contribution

The remaining amount — after the subsidy and the applicant’s own contribution — is provided as a term loan by the bank. This subsidy (called margin money) is kept in a lock-in account for three years. If the business runs successfully and loan repayments remain consistent, the subsidy amount is adjusted toward the outstanding loan at the end of the lock-in period.

PMEGP Loan Interest Rate: What to Expect

One of the most searched questions around this scheme is about the PMEGP loan interest rate. The honest answer is that the interest rate is not fixed by the government — it varies depending on the lending bank and is generally aligned with their existing MSME loan rates.

Typically, the interest rates fall in the range of 9% to 12% per annum, depending on the bank’s internal policies, the borrower’s credit profile, and the project type. Applicants are advised to compare rates across the PMEGP loan bank list before finalizing their preferred lender.

Loans up to ₹10 lakh are covered under CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises), meaning no collateral is required for such amounts. This is a significant benefit for first-time entrepreneurs who may not own property to pledge as security.

PMEGP Loan Bank List 2021 and 2022: Which Banks Participate?

The PMEGP loan bank list 2021 and PMEGP loan bank list 2022 largely remain consistent, as all major nationalized and scheduled commercial banks are empaneled under the scheme. These include:

- State Bank of India (SBI)

- Punjab National Bank (PNB)

- Bank of Baroda

- Canara Bank

- Union Bank of India

- Indian Bank

- Bank of India

- Regional Rural Banks (RRBs) and cooperative banks in select states

When submitting an application, the applicant needs to choose a bank branch that is MSME-friendly and ideally located near the proposed unit. A branch that is familiar with government-linked loan schemes tends to process applications more efficiently.

PMEGP Loan Documents Required

Having the right paperwork ready can significantly speed up the process. Here is a list of PMEGP loan documents that are typically required:

- Aadhaar card or Voter ID (age and residence proof)

- Passport-size photographs

- PAN card

- Educational certificate (8th pass certificate or above, depending on project cost)

- Detailed Project Report (DPR) — this is arguably the most critical document

- Bank account details and KYC documents

- Caste certificate (for SC/ST/OBC and other special category applicants)

- Any relevant business licenses or NOCs

The Detailed Project Report (DPR) deserves special attention. Banks and nodal agencies use this document to evaluate the viability of the proposed business. A poorly written DPR is one of the top reasons applications get rejected or delayed.

How to Apply for PMEGP Loan: Step-by-Step Process

Now comes the part everyone is most curious about — the PMEGP loan process and how to get started. The entire application is handled online through the official KVIC e-portal.

PMEGP Loan Apply Online

Here’s a step-by-step walkthrough on how to do a PMEGP loan apply online:

Step 1: Visit the official KVIC website at kviconline.gov.in and navigate to the PMEGP e-portal

Step 2: Click on “Online Application Form for Individual” (or Non-Individual for organizations)

Step 3: Fill in the registration form with personal details — Aadhaar number, full name, state, district, gender, educational qualification, mobile number, email address, PAN number, and date of birth

Step 4: Enter proposed project details — business activity, location (rural or urban), estimated project cost, capital expenditure, and working capital breakdown

Step 5: Upload all required documents including Aadhaar, educational proof, project report, and caste certificate if applicable

Step 6: Select the implementing agency (KVIC, KVIB, or DIC) and choose the preferred bank branch

Step 7: Click “Save Applicant Data,” note the Application ID, and print a copy to submit to the nearest nodal agency office

PMEGP Loan Apply Online Login

For those who have already registered, the PMEGP loan apply online login option is available on the official portal. Returning applicants can log in using their registered mobile number and credentials to check application status, upload additional documents, or apply for a second loan.

PMEGP Loan Application: What Happens After Submission

Once the PMEGP loan application is submitted, here’s what the process looks like:

- The application goes to the District Level Task Force Committee (DLTFC) for initial screening and interview

- Shortlisted applications are forwarded to the chosen bank for project appraisal

- The bank sanctions a term loan along with working capital based on the project cost

- After loan sanction, the beneficiary must complete a free 15-day Entrepreneurship Development Programme (EDP) training — this is mandatory

- The EDP certificate must be submitted to both the bank and the implementing agency

- The government then releases the margin money subsidy into a separate account linked to the loan

- The business unit must be established and operations must begin within a stipulated time

PMEGP Loan Status: How to Track the Application

Applicants don’t need to keep calling offices or visiting banks to know what’s happening with their file. The PMEGP loan status can be tracked easily online.

Here’s how:

- Visit the official PMEGP e-portal

- Click on “Track Application Status”

- Enter the Application ID received at the time of registration

- The current status of the application will be displayed on screen

This digital tracking feature is part of the government’s push toward transparency and ease-of-access under the PMEGP loan govt initiative.

PMEGP Loan Calculator: Estimating Costs and Subsidy

Before applying, it’s smart to use a PMEGP loan calculator to get a rough estimate of how much subsidy one can expect, how much the bank loan will be, and what the self-contribution requirement looks like.

Here’s a simple example:

Scenario: A woman entrepreneur from a rural area applying for a ₹10 lakh manufacturing project under Special Category

- Subsidy (35%): ₹3.5 lakh

- Self-contribution (5%): ₹50,000

- Bank loan: ₹6 lakh

Scenario: A general category applicant in an urban area with a ₹10 lakh project

- Subsidy (15%): ₹1.5 lakh

- Self-contribution (10%): ₹1 lakh

- Bank loan: ₹7.5 lakh

Several third-party and government-affiliated websites offer a basic PMEGP loan calculator tool where these values can be plugged in automatically.

PMEGP Personal Loan: Is It Different?

A common point of confusion is whether there’s a PMEGP personal loan option separate from the business loan. The answer is no — PMEGP is exclusively a business loan scheme. It does not offer personal loans for individual consumption, education, or personal expenses.

The loan is tied entirely to a specific business project and is disbursed in alignment with the project’s capital and working capital needs. Those looking for personal financing should explore other government schemes that cater to individual needs.

PMEGP Loan in Hindi: Reaching Every Entrepreneur

To ensure the scheme reaches every corner of the country, information about PMEGP loan Hindi resources is widely available. The official KVIC website and the PMEGP e-portal provide guidelines, application forms, and project reports in Hindi, making it accessible for non-English speakers in tier-2 and tier-3 cities, as well as rural areas.

Several state-level DICs also provide assistance in regional languages during the interview and application stages, ensuring no eligible entrepreneur is left behind due to a language barrier.

PMEGP Loan Govt Gyan: Reliable Sources to Learn More

For those who prefer video-based or simplified explanations, PMEGP loan Govt Gyan refers to the type of accessible, citizen-friendly government content that breaks down scheme details in everyday language. The official YouTube channels of KVIC and MoMSME, along with the Jan Samarth portal, serve as great starting points for understanding the scheme in depth without wading through dense official circulars.

Common Mistakes to Avoid When Applying

Even with a solid business idea and proper documents, some applicants run into avoidable problems. Here are the most common ones:

- Submitting a weak or generic Detailed Project Report (DPR)

- Applying for an existing or already-running business

- Choosing the wrong implementing agency for the type of business

- Skipping EDP training after loan sanction

- Not tracking application status regularly, leading to missed deadlines

- Providing incorrect bank branch details during registration

Frequently Asked Questions

Can someone apply for a PMEGP loan a second time?

Yes. Existing PMEGP beneficiaries whose units are running well and whose first loan has been repaid can apply for a second loan for business upgradation through the PMEGP portal.

Is there an age limit for applying?

The minimum age is 18. There is no published upper age limit for most categories.

How long does the approval take?

Typically, the process takes between 2 to 3 months from the date of application submission, subject to document verification and bank processing time.

Is collateral required?

No collateral is required for loans up to ₹10 lakh under CGTMSE coverage.

Conclusion

The PMEGP loan is one of India’s most inclusive and well-structured entrepreneurship support schemes. Whether someone is a first-generation business owner in a small town or a skilled artisan looking to scale up, this scheme offers real financial leverage through a mix of a bank loan and government subsidy. With the enhanced limits, digital application process, and extended programme timeline through 2025–26, there has never been a better time to explore what the PMEGP loan yojana can do.

Anyone interested can visit the official KVIC portal, use the PMEGP loan calculator to estimate their benefit, and begin their PMEGP loan apply online journey today.

Also Read: Small Business Insurance Quote Everything You Need to Know Before You Buy