FHA Modular Home Loan Requirements, Loan Limits & How to Qualify in 2026

Introduction

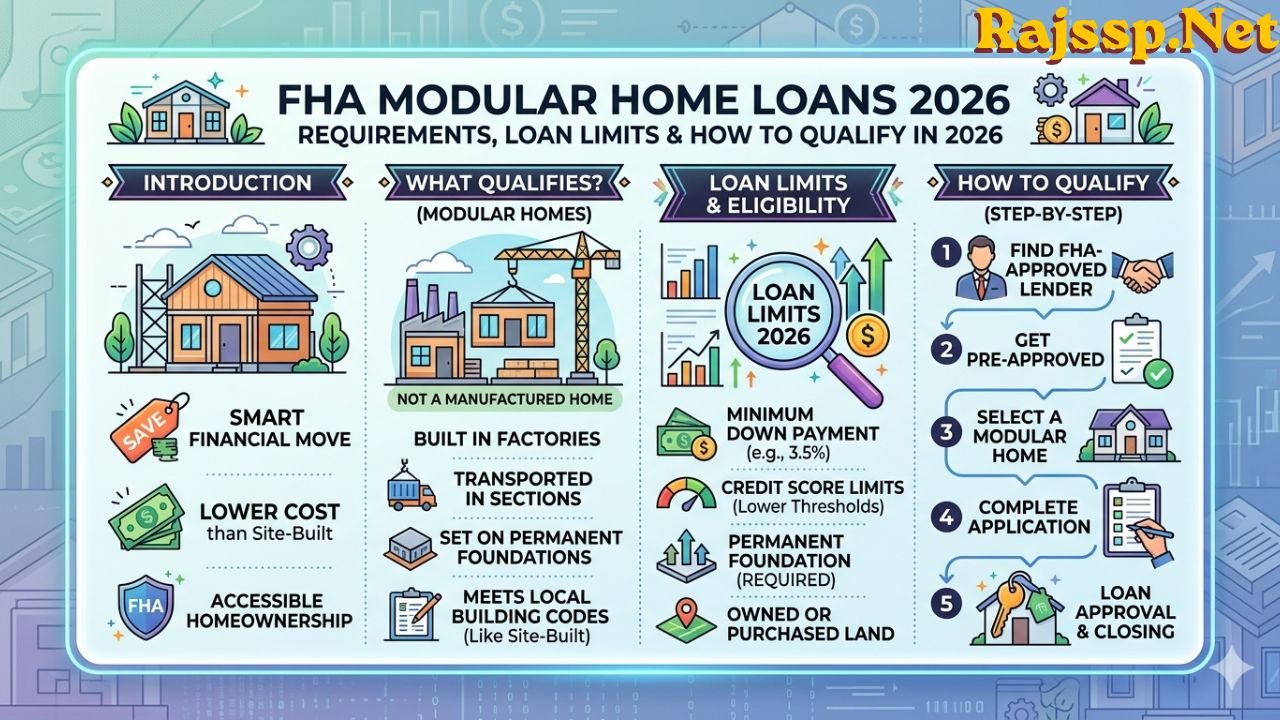

Buying a home doesn’t have to break the bank — and that’s exactly where modular homes shine. Compared to traditional site-built homes, modular homes can cost significantly less while offering the same level of quality and comfort. For buyers who want to stretch their budget even further, pairing a modular home with an FHA modular home loan is one of the smartest financial moves available today.

An FHA modular home loan is a mortgage backed by the Federal Housing Administration (FHA) that helps buyers finance the purchase of a modular home. These loans are especially popular among first-time homebuyers because they come with lower credit score thresholds, smaller down payment requirements, and competitive interest rates — all of which make homeownership more accessible to a broader range of people.

This guide covers everything a buyer needs to know about FHA loans for modular homes in 2026 — from what qualifies as a modular home, to loan limits, eligibility requirements, and how to apply step by step.

What Is a Modular Home? (And How It Differs from Manufactured/Mobile Homes)

Before diving into financing, it helps to understand exactly what type of home is being discussed — because “modular,” “manufactured,” and “mobile” are three very different things in the eyes of lenders and the FHA.

Modular Homes

A modular home is built in sections inside a factory, then transported to the property and assembled on a permanent foundation. These homes are constructed to meet local or state building codes — the same codes that apply to traditional stick-built homes. Once assembled, they’re virtually indistinguishable from a home built entirely on-site.

Manufactured Homes

Manufactured homes are also factory-built, but they’re transported on a permanent steel chassis and governed by the U.S. Department of Housing and Urban Development (HUD) standards rather than local building codes. These are commonly referred to as “HUD-code homes.”

Mobile Homes

Technically, mobile homes are any prefabricated homes built before June 15, 1976 — the date when HUD established its Manufactured Home Construction and Safety Standards. Because they predate federal safety regulations, mobile homes are not eligible for FHA loans under any circumstances.

Quick Comparison Table

| Feature | Modular Home | Manufactured Home | Mobile Home |

|---|---|---|---|

| Built in a factory | Yes | Yes | Yes |

| Governed by | Local/state codes | HUD code | No federal standard |

| Permanent foundation required | Yes | Sometimes | No |

| FHA eligible | Yes | Yes (with conditions) | No |

| Built after June 15, 1976 | Yes | Yes | No |

Can You Get an FHA Loan for a Modular Home?

The short answer is yes — and it’s actually more straightforward than many buyers expect.

When someone asks, “Can you buy a modular home with an FHA loan?” — the answer is a confident yes. Modular homes are treated as real property by lenders and the FHA because they are permanently affixed to a foundation, built to local building codes, and typically sold together with the land they sit on. This means no special HUD-specific guidelines apply to modular homes the way they do to manufactured homes.

Because modular homes meet the same construction and safety standards as site-built homes, they qualify for standard FHA financing. Buyers don’t need to navigate a separate set of modular-specific rules — the standard FHA loan process applies from start to finish.

The key distinction to remember: modular homes follow local building codes, while manufactured homes follow the federal HUD code. That difference makes modular home financing far simpler.

FHA Modular Home Loan Requirements

Whether someone is exploring an FHA loan for modular home purchase or looking to refinance, there are requirements on both the property side and the borrower side that must be met.

Property Requirements

For a modular home to be eligible for FHA financing, it must meet the following criteria:

- Permanently affixed to a foundation: The home must be fixed to the land — it cannot be movable or sitting on blocks.

- Land ownership required: The borrower must own the land the home sits on. FHA loans on modular homes cannot be used to finance homes on leased land.

- Standard FHA appraisal: The property must pass a standard FHA appraisal. Unlike manufactured homes, modular homes don’t require any special modular-specific inspections.

- Primary residence: The home must serve as the borrower’s primary place of residence — FHA loans are not available for vacation homes or investment properties.

Borrower Requirements

On the borrower side, FHA loan eligibility for modular homes follows standard FHA guidelines:

- Credit score and down payment: A credit score of 580 or higher qualifies for a 3.5% down payment. Borrowers with scores between 500 and 579 will need to put down at least 10%.

- Debt-to-income (DTI) ratio: Lenders typically want to see a DTI of 43% or lower. In some cases, exceptions are made for borrowers with strong credit scores or larger down payments.

- Stable income and employment: A consistent, verifiable employment history is required. Lenders will typically review the past two years of income documentation.

- Citizenship: Applicants must be U.S. citizens or eligible non-citizens.

Lender Requirements

Not all lenders offer FHA loans for modular homes, so finding the right lending partner matters. All FHA loans must be issued through FHA-approved lenders. Additionally, while FHA guidelines set a minimum credit score of 580, most lenders who offer modular home financing in practice require a minimum score of 640. It’s always worth comparing multiple lenders to find the best fit.

FHA Loan Types for Modular Homes

There are two primary FHA loan programs relevant to modular home buyers.

FHA Title II Loan (Most Common for Modular Homes)

The Title II loan is the standard FHA mortgage product and the most commonly used option for FHA loans for modular homes. These are fixed-rate loans designed for financing homes and land purchased together, with loan terms of either 15 or 30 years.

In 2026, FHA Title II loan limits range from $541,288 in lower-cost counties to $1,249,125 in high-cost areas for one-unit properties. This range gives buyers in most markets more than enough room to finance a quality modular home with land.

This loan type is best suited for buyers who already own land or are purchasing land and the modular home together as a package.

FHA One-Time Close Construction Loan

For buyers who want to build a brand-new modular home from the ground up, the FHA One-Time Close construction loan is an excellent option. The FHA allows borrowers to use this construction-to-permanent financing program on modular homes.

With this program, there’s a single loan closing that covers both the construction phase and the permanent mortgage — simplifying the process and reducing closing costs. This option is ideal for buyers who are working with a modular home builder and want one seamless financing experience.

FHA Modular Home Loan Limits (2026)

Understanding loan limits is essential before beginning the homebuying process. In 2026, the baseline conforming loan limit is $832,750, while FHA Title II limits sit at a floor of $541,288 and a ceiling of $1,249,125 for one-unit properties.

Here’s what buyers should know about limits:

- Limits vary by county: Every county has its own FHA loan limit based on local home prices. Buyers in high-cost metros will have access to higher limits.

- High-cost area exceptions: States like Alaska, Hawaii, and certain metropolitan regions have significantly higher limits — sometimes reaching or exceeding the $1,249,125 ceiling.

- How to check limits: The HUD website provides an official FHA loan limit lookup tool where buyers can enter their county to find the exact limit that applies to them.

Buyers are encouraged to check the limits in their specific area before setting a budget.

How to Apply for an FHA Modular Home Loan

Applying for an FHA loan on modular home purchases follows a clear, manageable process. Here’s a step-by-step breakdown:

Step 1 — Check Credit Score and DTI Ratio Before anything else, review credit reports and calculate the debt-to-income ratio. Knowing where things stand financially helps set realistic expectations and identify any areas to improve before applying.

Step 2 — Get Pre-Approved by an FHA-Approved Lender Pre-approval tells buyers how much they can borrow and shows sellers they’re serious. It also speeds up the process once a home is found.

Step 3 — Choose a Modular Home and Confirm FHA Eligibility Select a modular home and verify it meets FHA property standards — permanently affixed to a foundation, built to local codes, and to be used as a primary residence.

Step 4 — Order an FHA Appraisal The lender will arrange for an FHA-approved appraiser to evaluate the property’s value and condition. This step ensures the home meets FHA’s minimum property requirements.

Step 5 — Underwriting and Final Loan Approval The lender’s underwriting team will review all financial documents, the appraisal report, and property details. This is where final decisions are made on loan approval.

Step 6 — Closing At closing, the buyer signs all final documents, pays closing costs, and receives the keys. For One-Time Close loans, this step also initiates the construction process.

Pros and Cons of an FHA Modular Home Loan

Like any financial product, an FHA modular home loan comes with its share of advantages and limitations. Here’s an honest look at both sides.

Pros

- Low down payment: Qualified buyers can put down as little as 3.5%, making it much easier to get into a home without a massive savings account.

- Flexible credit requirements: FHA accepts lower credit scores compared to conventional loans, opening the door for more buyers.

- Competitive interest rates: FHA-backed loans typically offer lower interest rates than non-government-backed alternatives.

- Lower construction costs: Modular homes can cost up to 20% less to build compared to site-built homes, and since costs are locked in before construction begins, buyers avoid the surprise expenses common with on-site construction.

- Same treatment as traditional homes: Because modular homes follow local building codes, they’re financed just like any other home — no extra hurdles or special programs required.

Cons

- Mortgage insurance premium (MIP): FHA loans require both an upfront MIP and an annual MIP, which adds to the overall loan cost.

- Land ownership required: Buyers who don’t already own land will need to purchase it, which adds to the total cost.

- Loan limits can be restrictive: In some high-cost markets, FHA limits may not fully cover the cost of land plus a modular home.

- Limited lender availability: Not every FHA-approved lender offers modular home loans, so finding the right lender may take some extra legwork.

FHA Modular Home Loan vs. Conventional Loan

Buyers sometimes wonder whether to pursue an FHA or conventional loan for their modular home. Here’s how the two compare:

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum down payment | 3.5% (580+ score) | 3%–5% (higher credit needed) |

| Minimum credit score | 580 (500 with 10% down) | Typically 620–640+ |

| Mortgage insurance | Required (MIP) | PMI required if <20% down |

| Loan limits (2026) | Up to $1,249,125 | Up to $806,500 (baseline) |

| Best for | Lower credit, smaller down payment | Higher credit, avoiding long-term MIP |

When FHA makes more sense: For buyers with credit scores in the 580–640 range or limited savings for a down payment, an FHA loan is usually the better path. The more forgiving qualification standards make homeownership achievable when conventional financing might not be an option.

When conventional may be better: Buyers with strong credit (700+) and a 20% down payment may prefer a conventional loan to avoid paying MIP for the life of the loan. Conventional loans also tend to have fewer restrictions on property types in some scenarios.

Frequently Asked Questions (FAQ)

Is a modular home the same as a manufactured home for FHA purposes?

No. Modular homes are built to local or state building codes and classified as real property. Manufactured homes follow the federal HUD code and have additional FHA requirements. The two are treated very differently in the lending process.

Do I need to own land to get an FHA modular home loan?

Yes. FHA loans for modular homes require the borrower to own the land. Unlike manufactured home financing under Title I, there’s no option to use leased land when financing a modular home.

What credit score do I need for an FHA loan for modular home purchase?

The FHA minimum is 580 for a 3.5% down payment. However, most lenders who offer modular home financing prefer a score of at least 640 in practice.

Are there special inspections required for modular homes?

No. Since modular homes are treated like site-built homes, only a standard FHA appraisal is required. There are no HUD-specific foundation inspections or certification label requirements like those for manufactured homes.

Can someone use an FHA loan to build a new modular home?

Absolutely. The FHA One-Time Close construction loan allows buyers to finance the construction and permanent mortgage of a new modular home in a single transaction with one closing.

Can you buy a modular home with an FHA loan if the builder is new?

Yes, as long as the home meets FHA property standards and is permanently affixed to land the borrower owns. Working with an experienced FHA-approved lender who understands modular home nuances is highly recommended.

Conclusion

For buyers looking for an affordable, quality path to homeownership, an FHA modular home loan checks a lot of boxes. Modular homes cost less to build, are constructed to the same standards as traditional homes, and qualify for standard FHA financing — which means lower down payments, flexible credit requirements, and competitive interest rates.

Whether someone is exploring an FHA loan for modular home for the first time or comparing options against conventional financing, the case for FHA is strong — especially for first-time buyers and those working with limited savings or rebuilding credit.

The best next step is to connect with an FHA-approved lender who specializes in modular home financing, get pre-approved, and start the journey toward owning a quality home at a price that makes sense.

Also Read: Renters Insurance Ohio Coverage, Costs & Best Providers (2026 Guide)