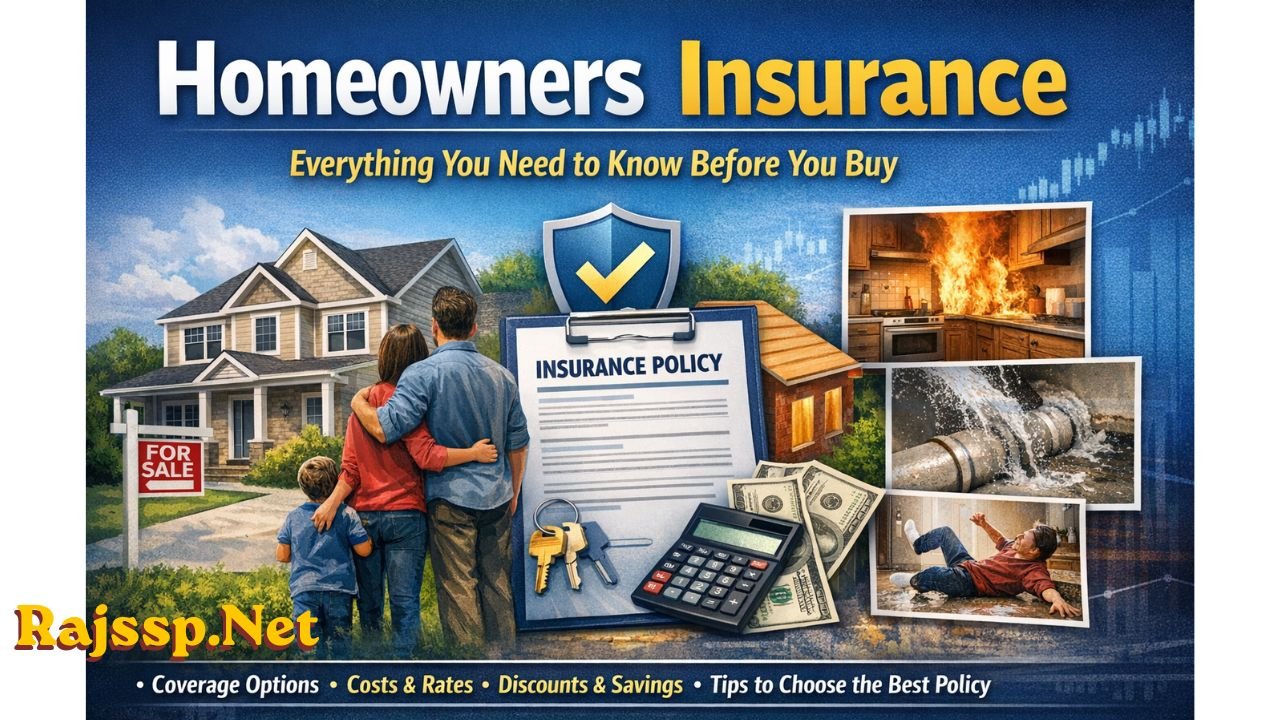

Homeowners Insurance Everything You Need to Know Before You Buy

Buying a home is one of the biggest financial decisions a person will ever make — and protecting it should be just as serious a priority. Homeowners insurance is the safety net that stands between a homeowner and financial disaster when the unexpected happens. Whether it is a burst pipe, a kitchen fire, or a liability lawsuit from a neighbor’s slip-and-fall, the right policy quietly does its job in the background — until you desperately need it.

This guide walks through everything a homeowner needs to understand: what the coverage actually includes, how policies differ, what affects pricing, and how to find the best deal without cutting corners.

What Is Homeowners Insurance and Why Does It Matter?

At its core, homeowner insurance is a contract between a policyholder and an insurance provider. The homeowner pays a regular premium, and in return, the insurer agrees to cover financial losses caused by specific events — things like fire, theft, windstorm damage, or accidental injuries on the property.

But it goes beyond just protecting the building. A solid homeowners insurance home policy also covers personal belongings inside the house, provides liability protection if someone gets injured on the premises, and pays for temporary housing if the home becomes uninhabitable after a covered event.

For anyone with a mortgage, it is not optional — lenders require it. But even for those who own their homes outright, going without coverage is a financial gamble that rarely pays off.

What Does a Standard Policy Cover?

Understanding what a homeowners insurance policy actually covers helps homeowners avoid nasty surprises at claim time. Most standard policies are broken into six distinct coverage types:

Dwelling Coverage (Coverage A) This covers the structure of the home itself — the walls, roof, floors, and built-in systems. If a fire tears through the kitchen or a hailstorm caves in the roof, dwelling coverage pays for the repairs or rebuild.

Other Structures (Coverage B) Detached garages, garden sheds, fences, and driveways fall under this category. It typically equals about 10% of the dwelling coverage limit.

Personal Property (Coverage C) Furniture, electronics, clothing, and everyday belongings are covered here. If a burglary cleans out the living room or a fire destroys everything inside, personal property coverage steps in.

Loss of Use (Coverage D) If a covered event makes the home temporarily unlivable, this coverage pays for hotel stays, restaurant meals, and other extra living costs while repairs are underway.

Personal Liability (Coverage E) This is the protection most people overlook — until they need it. If a visitor trips on a broken step and sues, personal liability coverage handles legal fees and potential settlements.

Medical Payments (Coverage F) For minor injuries to guests on the property, this coverage pays medical bills directly — no lawsuit required.

Types of Homeowners Insurance Policies (HO-1 Through HO-8)

Not all homeowners are in the same situation, which is why there are multiple policy types designed for different needs.

HO-3: The Most Common Policy The HO-3 is what most homeowners carry. It provides open-peril coverage for the dwelling — meaning everything is covered unless it is specifically excluded — and named-peril coverage for personal belongings. It strikes a solid balance between broad protection and affordable premiums.

HO-5: Maximum Coverage The HO-5 offers open-peril coverage for both the structure and personal property. It is ideal for high-value homes and homeowners who want the broadest possible protection.

HO-6: Condo Owners Condo owners need a different type of policy since the building’s exterior is typically covered by the HOA’s master policy. HO-6 covers the unit’s interior, personal property, and personal liability.

HO-8: Older and Historic Homes HO-8 is designed for older homes where the cost to rebuild using original materials would far exceed the home’s market value. It pays out on an actual cash value basis rather than replacement cost.

What Is and Is Not Covered

One of the most important things to understand about any homeowners insurance company policy is what it specifically excludes. Many homeowners are shocked to discover after a disaster that their policy does not cover the very event that occurred.

Commonly Covered Perils:

- Fire and smoke damage

- Lightning strikes

- Windstorm and hail

- Theft and vandalism

- Water damage from burst or frozen pipes

- Falling objects

Standard Exclusions:

- Flood damage (requires a separate flood insurance policy)

- Earthquake damage (requires an add-on or separate policy)

- Normal wear and tear

- Mold caused by long-term neglect

- Pest or rodent infestations

- Intentional damage

For homeowners in flood-prone areas, this exclusion is critically important. Flood insurance is available through the National Flood Insurance Program (NFIP) or private insurers and must be purchased separately. Similarly, those in earthquake-prone regions — particularly in homeowners insurance California territory — should seriously consider adding earthquake coverage to their protection plan.

Homeowners Insurance in California: Special Considerations

Residents searching for homeowners insurance California policies face a uniquely challenging market. Wildfires, earthquakes, and severe droughts have made California one of the most difficult states for insurance coverage in recent years. Several major insurers have reduced their footprint in the state, which has driven up prices and limited options for many residents.

California homeowners often need to consider:

- FAIR Plan insurance — a last-resort pool for those who cannot find private coverage

- Separate earthquake riders or policies — the California Earthquake Authority (CEA) is a primary source

- Wildfire mitigation discounts — insurers may offer reduced rates for homes with fire-resistant features like ember-resistant venting, Class A roofing, and defensible space

Shopping around and comparing a homeowners insurance quote from multiple providers is especially important in California, where rates and availability can vary dramatically from one ZIP code to the next.

Bundling Car and Homeowners Insurance

One of the easiest and most popular ways to save money is by combining car and homeowners insurance under a single provider. Insurers reward this loyalty with what is commonly called a bundling discount — often ranging from 5% to 25% off both policies.

Homeowners car insurance bundles simplify life in other ways too. Instead of juggling two separate insurers, two separate billing cycles, and two separate customer service phone numbers, everything lives under one roof. In the event of a claim that involves both policies — like a car crashing into the home — having a single insurer can also make the claims process far less complicated.

Top Homeowners Insurance Companies to Know

Allstate Insurance Quote Homeowners

Allstate is one of the most recognized names in the industry. Getting an allstate insurance quote homeowners is straightforward through their website or a local agent. Allstate is known for its wide range of coverage options, extensive agent network, and useful digital tools like the digital locker for tracking personal property. They also offer several discounts, including claim-free, multi-policy, and new home discounts.

Liberty Mutual Homeowners Insurance

Liberty Mutual homeowners insurance is popular among homeowners who want flexible customization options. Their policies allow policyholders to tailor coverage with add-ons like inflation protection, blanket jewelry coverage, and water backup protection. Liberty Mutual also features a straightforward online quote process and a well-rated mobile app.

GEICO Homeowners Insurance

GEICO homeowners insurance works a little differently from the other two — GEICO acts as a marketplace that connects customers with underwriting partners rather than writing policies directly. Still, getting a geico homeowners insurance quote through their platform is quick and easy, and the company leverages its reputation for customer service and competitive pricing. Those who already have GEICO auto coverage will find the bundling process seamless.

How to Get a Homeowners Insurance Quote

Getting a homeowners insurance quote — or better yet, several of them — is the smartest first step toward finding the right policy. Here is how the process typically works:

Step 1: Gather the basics Insurers will ask for the home’s address, square footage, year built, construction materials, roof age, and any recent upgrades.

Step 2: Decide on coverage levels Determine the dwelling coverage needed (ideally enough to fully rebuild the home), the personal property limit, and the preferred deductible.

Step 3: Request a homeowners insurance quotation A homeowners insurance quotation can be obtained online in minutes from most major insurers, or by calling a local agent. Getting at least three to five quotes allows for a meaningful comparison.

Step 4: Compare apples to apples When reviewing a homeowners insurance quotes list, make sure each quote reflects the same coverage limits, deductibles, and endorsements — otherwise, the comparison is not meaningful.

Step 5: Check the insurer’s ratings Look at AM Best financial strength ratings and J.D. Power customer satisfaction scores before committing to any provider.

Finding the Best Homeowners Insurance

What counts as the best homeowners insurance depends heavily on individual priorities. For some homeowners, the best policy is the one with the broadest coverage. For others, it is the one with the most responsive claims team. For many, it is simply the one that delivers solid protection at a fair price.

The best homeowners insurance options generally share a few traits in common:

- Strong financial ratings (A or better from AM Best)

- Clear policy language with no surprising exclusions

- Competitive pricing for the coverage level provided

- Positive customer service and claims satisfaction scores

- A range of discounts that apply to the homeowner’s situation

Finding the Cheapest Homeowners Insurance Without Sacrificing Coverage

Everyone wants the cheapest homeowners insurance available — but cheap should never mean inadequate. The good news is that smart shopping can bring the cost of a quality policy down significantly without gutting the coverage.

Strategies for Finding Cheap Homeowners Insurance

Raise the deductible. Opting for a $2,000 or $2,500 deductible instead of $500 can dramatically lower the annual premium. The key is making sure that higher deductible is actually affordable if a claim arises.

Bundle policies. As mentioned, combining auto and home coverage under one insurer is one of the most reliable ways to find cheap homeowners insurance with meaningful discounts.

Improve home security. Installing monitored alarm systems, deadbolts, smoke detectors, and smart home devices often qualifies for discounts with many insurers.

Maintain a clean claims history. Avoiding small claims keeps the claims history clean, which helps keep premiums lower over time.

Ask about loyalty discounts. Staying with the same insurer for multiple years can trigger loyalty-based premium reductions.

How to Find Homeowners Insurance Near Me

Searching for homeowners insurance near me is a natural starting point for many first-time homebuyers. Local independent insurance agents are often the most helpful resource for this search — they work with multiple carriers and can run comparison quotes tailored to the local market and specific home characteristics.

For those who prefer the digital route, most national insurers allow visitors to enter a ZIP code on their website and receive a localized homeowners insurance quotation in minutes. State-specific insurance department websites can also point homeowners toward licensed providers operating in their area.

Factors That Affect Homeowners Insurance Premiums

Understanding what drives the cost of a policy helps homeowners make smarter decisions when shopping.

Location. Homes in areas prone to hurricanes, wildfires, tornadoes, or flooding typically cost more to insure. Being close to a fire station or fire hydrant can actually lower premiums.

Home age and construction. Older homes with outdated electrical, plumbing, or roofing systems are considered higher risk and cost more to insure.

Roof condition. The roof is one of the first things insurers look at. A newer roof — especially one made of impact-resistant materials — can earn meaningful discounts.

Credit-based insurance score. Most states allow insurers to use credit information as a pricing factor. Maintaining a strong credit profile can help keep premiums competitive.

Claims history. Prior claims show up in the CLUE (Comprehensive Loss Underwriting Exchange) report. A history of frequent claims signals higher risk and results in higher premiums.

Filing a Homeowners Insurance Claim: Step by Step

Knowing how the claims process works before disaster strikes makes a stressful situation much more manageable.

Document everything immediately. Take photos and videos of all damage before making any temporary repairs.

Notify the insurer promptly. Most policies require notification within a reasonable timeframe after a loss. Delays can complicate or even jeopardize a claim.

Make temporary repairs if needed. To prevent further damage, homeowners can make temporary fixes — just keep all receipts, as these costs are typically reimbursable.

Meet with the adjuster. The insurer will send a claims adjuster to assess the damage. Having a detailed home inventory ready speeds up this process considerably.

Review the settlement offer carefully. If the settlement seems too low, homeowners have options — invoking the appraisal clause, hiring a public adjuster, or filing a complaint with the state insurance commissioner.

Annual Policy Review: Do Not Set It and Forget It

A homeowners insurance home policy should be reviewed every year — not just when it automatically renews. Life changes like major renovations, new high-value purchases, or a change in home-based business activity can all create coverage gaps if the policy is not updated accordingly.

Getting a fresh homeowners insurance quotes comparison every year or two also ensures the homeowner is not overpaying compared to what competitors now offer.

Common Mistakes to Avoid

- Underinsuring the home. Insuring based on market value rather than rebuild cost is a common and costly mistake.

- Skipping flood insurance. Standard policies do not cover floods — period.

- Ignoring liability limits. The default liability limit ($100,000) may be far too low for many households. Umbrella policies can fill this gap affordably.

- Not reading the exclusions. The exclusions section of a policy is just as important as the declarations page.

Final Thoughts

Homeowners insurance is not just a box to check at closing — it is an active, living part of a homeowner’s financial plan. Whether someone is searching for the best homeowners insurance, getting their first allstate insurance quote homeowners, exploring liberty mutual homeowners insurance options, or hunting for the cheapest homeowners insurance in their ZIP code, the process rewards those who take the time to understand what they are buying.

The right policy from the right homeowners insurance company provides far more than financial reimbursement after a loss — it provides peace of mind that the place called home is protected, no matter what happens next.

Also Read: Rushmore Loan Management Services A Complete Guide for Borrowers