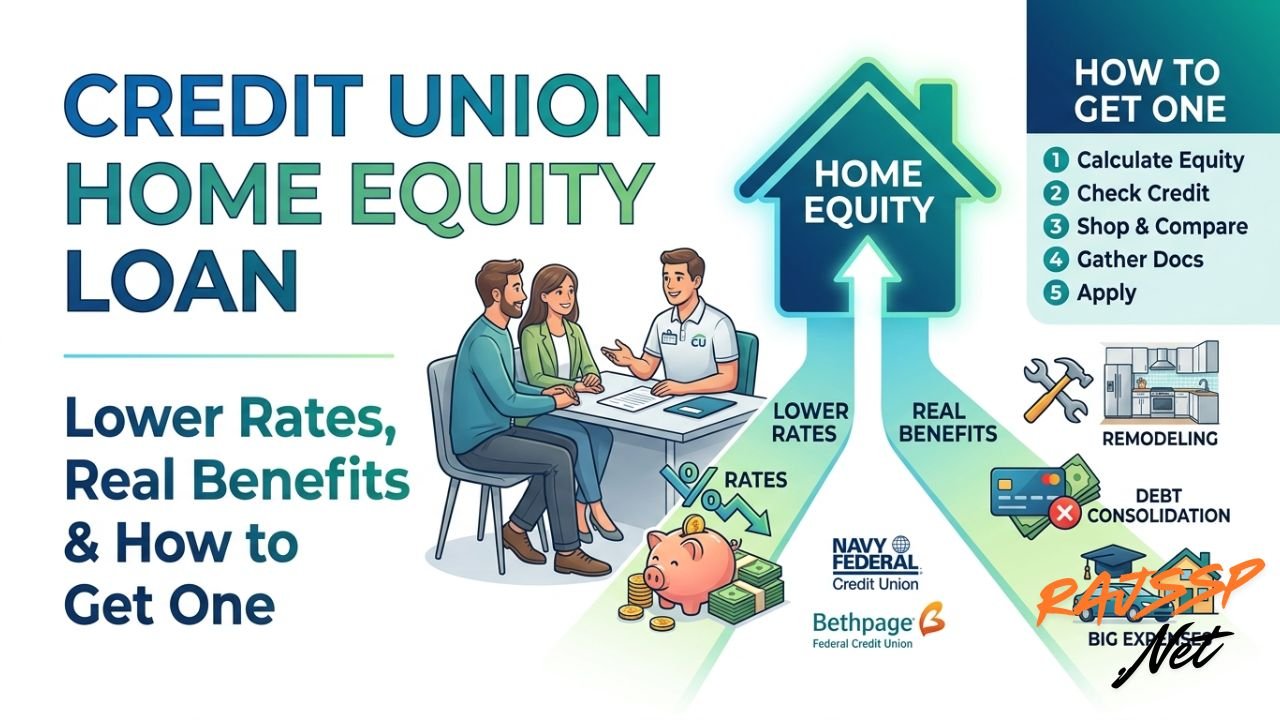

Credit Union Home Equity Loan: Lower Rates, Real Benefits & How to Get One

If someone has a decent amount of home equity and is wondering what to do with it, a credit union home equity loan might be one of the smartest financial moves they can make. Whether it is a kitchen remodel, paying off high-interest debt, or covering a big life expense, tapping into home equity through a credit union often comes with perks that traditional banks simply cannot match.

This guide breaks down everything a homeowner needs to know — from how these loans work and what rates look like, to how institutions like Navy Federal and Bethpage Federal Credit Union stand out from the crowd.

What Is a Home Equity Loan from a Credit Union?

A home equity loan is essentially a second mortgage. A homeowner borrows a lump sum against the equity they have built up in their property, and then repays it over time at a fixed interest rate. The amount someone can borrow typically depends on their equity, credit score, and income.

So, what makes a home equity loan credit union option different from going to a bank?

The answer lies in the structure of credit unions themselves. Unlike banks, credit unions are member-owned, not-for-profit financial cooperatives. That means profits get returned to members in the form of lower loan rates, fewer fees, and better service — rather than going to outside shareholders. For someone shopping for a home equity loan, this structure can translate into meaningful savings over the life of the loan.

Why Choose a Credit Union Over a Bank for a Home Equity Loan?

There are several reasons why more homeowners are turning to credit unions when it comes time to borrow against their home:

Lower Interest Rates Because credit unions are not driven by profit, they tend to offer interest rates that are noticeably lower than what traditional banks advertise. Even a half-point difference in rate can save thousands of dollars over a 10 or 15-year loan term.

Reduced Fees Many credit unions charge little to no origination fees on home equity loans. Closing costs also tend to be lower, which means more of the borrowed money actually goes toward the intended purpose.

Flexible Underwriting Credit unions often look at the full picture of a borrower’s financial situation rather than relying solely on automated scoring systems. Someone with a strong payment history but a slightly lower credit score may find more success at a credit union.

Personalized Service Dealing with a local loan officer who actually knows the community is a different experience than calling an 800 number. Credit unions are known for treating their members like people, not account numbers.

Navy Federal Credit Union Home Equity Loan Rates

For active-duty military members, veterans, and their families, Navy Federal Credit Union home equity loan rates are worth a serious look. Navy Federal is the largest credit union in the United States, and it has built a strong reputation for serving those who serve the country.

Navy Federal offers home equity loans with competitive fixed rates, and members often report that the application process is straightforward and well-supported. Their rates can vary based on loan term, the borrower’s credit profile, and the amount of equity available. Typically, members can borrow against a significant portion of their home’s value, often up to 100% combined loan-to-value in certain programs — a feature that is hard to find at most traditional lenders.

It is worth noting that Navy Federal membership is limited to military members, veterans, Department of Defense employees, and their family members. For those who qualify, however, it is one of the most competitive home equity loan options on the market.

Key highlights of Navy Federal’s home equity loan program:

- Fixed interest rates with predictable monthly payments

- No application or origination fees in many cases

- Loan terms ranging from 5 to 20 years

- Online application with dedicated loan officers available

Bethpage Federal Credit Union Home Equity Loan

Another strong option for homeowners — particularly those in New York — is the Bethpage Federal Credit Union home equity loan program. Bethpage Federal is one of the largest credit unions on the East Coast and has earned a loyal following for its competitive rates and member-friendly approach.

Bethpage offers both home equity loans and home equity lines of credit (HELOCs), giving members flexibility depending on their borrowing needs. Their home equity loan product typically features fixed rates, predictable payment schedules, and a streamlined application process.

One of the standout features of Bethpage is that joining is relatively easy — anyone can become a member by opening a savings account with a small deposit. That accessibility makes it a viable option for homeowners who are not already credit union members but want to explore better loan terms.

What borrowers generally appreciate about Bethpage Federal:

- Competitive fixed rates on home equity loans

- Options for both lump-sum loans and revolving credit lines

- Low or no closing costs on select products

- Strong digital banking tools for managing the loan

How Much Can Someone Borrow with a Credit Union Home Equity Loan?

The borrowing amount depends on a few key factors:

Loan-to-Value (LTV) Ratio Most credit unions allow borrowers to access up to 80–90% of their home’s appraised value, minus the outstanding mortgage balance. Some, like Navy Federal, may go higher for qualified members.

Credit Score A credit score of 680 or above typically unlocks the best rates and highest borrowing limits. That said, many credit unions are willing to work with scores in the 620–660 range depending on the overall application.

Debt-to-Income (DTI) Ratio Lenders want to see that a borrower’s total monthly debt payments do not exceed roughly 43% of their gross monthly income. A lower DTI signals financial stability and often results in better loan terms.

Equity Available The more equity a homeowner has built up, the more they can potentially borrow. Someone who has owned their home for many years or made extra mortgage payments may find themselves with a strong borrowing position.

Common Reasons People Use a Home Equity Loan

A credit union home equity loan is a versatile financial tool. Here are some of the most common ways homeowners put it to use:

- Home renovations: Kitchens, bathrooms, and additions are popular projects that can also increase the home’s resale value.

- Debt consolidation: Replacing high-interest credit card balances with a lower-rate home equity loan can reduce monthly payments significantly.

- Education costs: Helping cover tuition for a child or funding continuing education for career advancement.

- Medical expenses: Managing unexpected or large healthcare bills without draining savings.

- Emergency reserves: Rebuilding a cash cushion after a major financial setback.

One thing to keep in mind: since the home serves as collateral, it is important to borrow only what is truly needed and have a solid repayment plan in place.

How to Apply for a Home Equity Loan at a Credit Union

The process is more straightforward than many people expect. Here is a general roadmap:

Step 1 — Become a Member If someone is not already a member of the credit union, they will need to join first. Eligibility requirements vary. Navy Federal requires a military or DoD connection, while Bethpage Federal is open to virtually anyone willing to open a savings account.

Step 2 — Check Home Equity and Credit Before applying, it helps to get a rough idea of the home’s current market value and subtract the remaining mortgage balance. Pulling a free credit report is also a good idea to catch any errors.

Step 3 — Gather Documents Lenders typically ask for recent pay stubs or tax returns, a copy of the mortgage statement, proof of homeowners insurance, and sometimes a recent property tax bill.

Step 4 — Submit the Application Most credit unions now offer online applications alongside in-person options. The process involves answering questions about income, employment, the property, and the intended use of funds.

Step 5 — Appraisal and Underwriting The credit union will likely order a home appraisal to confirm the property’s current value. Underwriting reviews the full financial picture and typically takes one to three weeks.

Step 6 — Closing Once approved, the borrower signs the loan documents. Federal law gives borrowers a three-day right of rescission, meaning they can cancel within three business days if they change their mind. After that period, the funds are disbursed.

From application to funding, the process typically takes between two and six weeks.

Pros and Cons to Consider

Pros:

- Lower rates compared to most banks

- Fixed monthly payments make budgeting easy

- Interest may be tax-deductible when used for home improvements (consult a tax advisor)

- Fewer and lower fees than typical bank loans

- Relationship-based service from credit union staff

Cons:

- Membership is required to access credit union products

- The home is used as collateral — default carries foreclosure risk

- Some credit unions have limited branch access or older online platforms

- Approval can be slower than big-bank automated systems

Frequently Asked Questions

Can someone get a credit union home equity loan with bad credit?

It depends on the credit union. Some are more flexible than traditional lenders and may approve applicants with scores in the 600–640 range if other factors — like low debt and strong income — look solid.

Is a home equity loan the same as a HELOC?

No. A home equity loan provides a lump sum at a fixed rate. A HELOC (Home Equity Line of Credit) works more like a credit card with a variable rate and a draw period. Both are available at most credit unions, including Bethpage Federal.

How long does it take to get approved?

The typical timeline is two to six weeks from application to funding, though some credit unions can move faster for well-prepared applicants.

Are there prepayment penalties?

Many credit unions do not charge prepayment penalties, but it is always worth confirming before signing. Navy Federal, for example, is known for borrower-friendly loan terms.

Do credit unions offer home equity loans on investment properties?

Some do, but it is less common. Most credit unions focus on primary residences, though some may consider second homes. It is best to ask directly.

Final Thoughts

For homeowners who want to make the most of their equity without overpaying in fees or interest, a credit union home equity loan is a genuinely compelling option. Whether someone chooses Navy Federal Credit Union for its military-focused benefits and flexible LTV terms, or Bethpage Federal Credit Union for its accessible membership and competitive fixed rates, the credit union model consistently puts more money back in borrowers’ pockets.

The key is doing the homework — comparing rates, understanding eligibility, and choosing a lender that fits both the financial situation and the long-term goals. A good home equity loan, used wisely, can be a powerful step toward financial progress.

Also Read: MaxLend Loans: Everything You Need to Know Before You Borrow